|

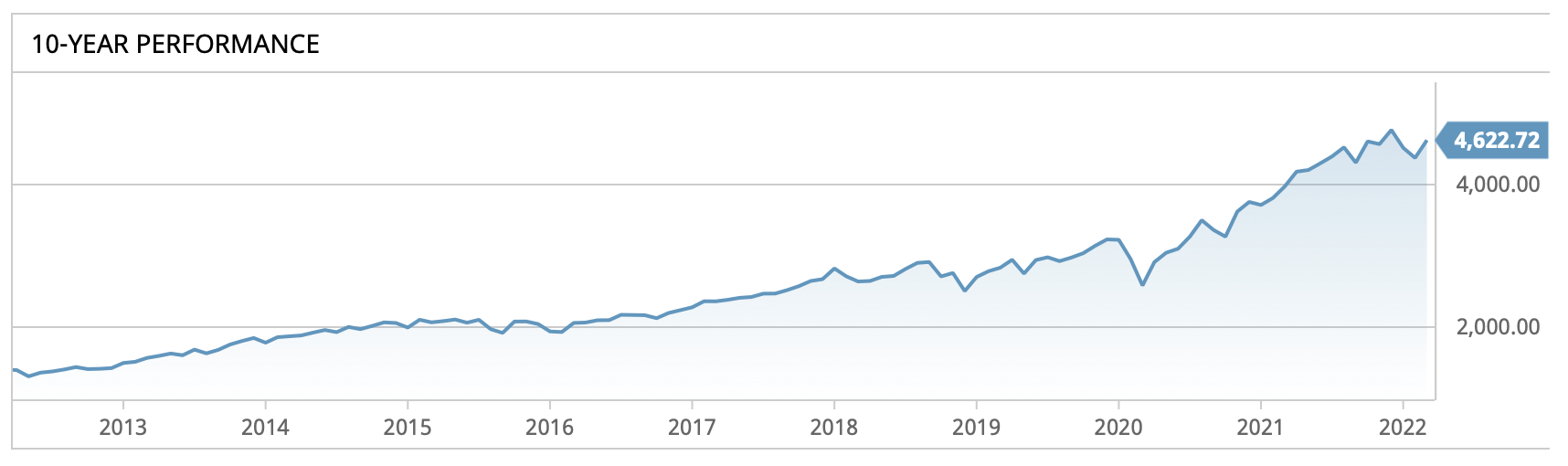

Looking on social media you could be forgiven for thinking that the only sensible way to invest is through an index fund. So many ‘finance gurus’ espouse the simplicity and low cost of just buying into a fund that tracks an index, often the S&P Index, that surely anything else would just be plain silly? For those of you that don’t know, an index fund is a fund that is constructed to match or track the components of a specific financial market. So rather than trying to beat the market, the fund just rides along on its wave. Many studies have shown that this approach can often do as well, if not better, than paying lots of clever financial types to construct an actively managed fund of specifically selected companies, that they believe will perform better than average. The S&P 500 is just one index that a fund can follow. The S&P 500’s full name is the Standard & Poor’s 500 index, which is an index of the top 500 companies in the United States and includes such behemoths as Apple, Amazon, Alphabet (Google) and Meta (Facebook). With big brand names like this you would expect this index to do well, and it does! Although S&P 500 index funds seem to dominate social media discussion, I guess because these top 500 US companies dominate the world stock markets, there are thousands of other index funds tracking all sorts of different markets. So if you want to track the world market or the UK market, for example, you can do this as well. So let’s just look at the S&P 500 briefly again. In recent years it has done very well in comparison to other markets, growing on average at around 10% each year over the last ten years. So this does look like a sensible investment option, surely?  The S&P 500 Well yes, it probably is. And whilst you can look at past data to give you an idea of what might happen in the future, in reality, without a time machine, we don’t know for sure what will happen in the next couple of years, let alone the next ten. What do all the finance sites say? ‘Past performance is no guarantee of future performance’, or words to that effect. They say this for a reason; things change, trends come and go, and markets can ‘wobble’.

And this is why, when I invest, I include plenty of diversification in my investments. And when I say ‘diversification’, I’m not just talking about different countries, but also different asset types as well. Because when some of you portfolio is taking a dip, a well diversified portfolio will have another asset type or another geographical area riding high. So index funds; yes they can be great, but if you are going to invest in them, make sure you diversify across asset types and geography when selecting them. Piling all you money into one index fund isn’t necessarily the best strategy. So why don’t I routinely invest in index funds? I believe that when investing you should be clear on your overall objective. If your objective is to grow overall value of your investment over the long term, then an index fund is a reasonable investment option to take. If you want a simple way to grow your portfolio with minimal input, then a group of diversified index funds may just be the thing for you. Set up a monthly direct debit to keep topping them up and watch your portfolio grow over the years. Forget about them, get on with your life and just do a check and rebalance every year or so. But what if you have a different objective? Like I do. I have given up my ‘normal’ day job. I retired, for want of a better term, about 3 years ago now and have since been living off income from my investments. To do this, I moved my investments from index funds into a number of actively managed funds, which do have slightly higher charges. However, on the plus side, these are giving me a regular income in the form of dividends and interest. I currently get just over 4% in ‘natural yield’ on these investments. That is to say, the dividends and interest alone are giving me £4,000 per year (around £350 per month) for every £100,000 I have invested. I can withdraw this as income without touching the original capital. Currently I can manage on less than the yield I’m getting and so some of the excess is being reinvested, as I’m sure I will get some years where the investments won't perform as well. This so called ‘Natural Yield’ approach does mean that you can never be certain of the amount of money you will ‘earn’ each year, but with a bit of planning and monitoring, your investments could provide an income for the rest of your life. As part of my strategy to diversify I have also put money into a number of other investments outside of the traditional equities and bond markets. There are a growing number of opportunities springing up, some of which may be higher risk, but some which actually may be slightly lower risk than many equity markets. The higher risk investment that I have invested some money in to is crypto currency. This is a very volatile market and not for the feint hearted. However, if you are brave enough, then there could be some significant long term gains here. I only invest small amounts here and that is as much through intrigue than anything else. As my confidence grows with time, I may invest a bit more. A slightly less risky option that gives me 5% is through an easy access account called Sterling Boost that Ziglu have recently launched. This is quite a new and innovative product where they converting your money to a stable-coin which is then lent out and you earn a portion of the interest that they get. Stable-coins are less volatile than other cryptocurrencies as they are linked directly to something of known value such as the US dollar, but still have all the advantages of crypto currencies by running on the blockchain. There are also a number of property based companies that I have investments with. These are essentially crowd funded property investments, either buying a part ownership in a property and receiving rental income or by supporting property developers through peer to peer lending. If you want to find out more about these then check out Proptee where you can buy fractions of properties through the magic of NFTs and Kuflink, where you can support property developers by lending money that is fully secured against the property being developed. These types of investments can pay out in the region of 6% -10% and so compare well to more traditional equity market investments. However, these are newer investments and so only time will tell if they were a worthwhile investment or not. Now where did I put that time-machine?

0 Comments

Leave a Reply. |

RSS Feed

RSS Feed