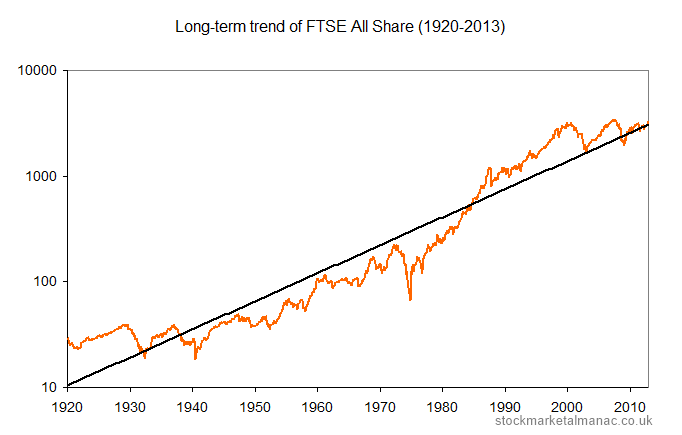

‘Less than 5% of Brits currently have a stocks and shares ISA’ according to Finder (https://www.finder.com/uk/stocks-and-shares-isa-statistics) And of those that have stocks and shares ISAs, the average amount invested is £9,331. This is despite the fact that the annual allowance for investing in a stocks and shares ISA is £20,000 and that any income or gains received is completely tax free. If you don’t feel that these statistics are shocking, then you should. Why is it that the people of the UK are not taking advantage of the benefits of these stocks and shares ISAs, when historically the amount you can grow your investment through such an ISA is so much better than leaving all your money in a traditional savings account earning minimal interest. I believe that one of the reasons that people shy away from stocks and shares in general is the ubiquitous warning you see with all of these types of products: “All investing should be regarded as long term. The value of investments can fall as well as rise, and you may get back less than you invested. Past performance is no guarantee of future results. Your capital is at risk” For many, this statement is a real turn-off for investing. Why would anyone want to put their money into something where the value could fall and they risk losing all their money? No thanks, I’ll put my money in the bank where it is safe. But let us look at the reality for a moment. Below is a graph of the last 100 years of the FTSE All Shares Index.  You see similar patterns in most other markets across the world. The trend is clearly one of continued growth, and usually at a rate which is significantly better than you can achieve in your bank’s standard savings account.

From the above graph you can see that there are some years that show a drop in value; and this is what the standard warning is all about. If you invest when the market is high and then withdraw within a short time frame where the market has temporarily dipped, then you will lose money. Investing therefore is about the ‘long game’. Money invested should stay invested. Leave it there and let it do it’s work, earning money for you. Apart from ‘time’, there are other ways to minimise the risk of a loss. The key way of minimising the risk is through diversification. By diversification we mean, invest in a number of different markets. If one market dips, then another market may be growing and offset this. You can also diversify through a number of different types of assets; company shares, corporate bonds etc. Many people might see this as added complexity that will put them off investing. But there are companies/apps that can help you with this, giving guidance or even having complete diversified portfolios already for you to invest in. One example is the app based investment broker, InvestEngine that for a small fee will put together a range of funds for you and manage them on an ongoing basis. However, one of the best things you can do, is to carry out a little bit of research yourself so that you can become confident at selecting a range of funds to invest in, through a broker such as Hargreaves Lansdown or Freetrade, where you have complete control over where you invest.

0 Comments

|

RSS Feed

RSS Feed