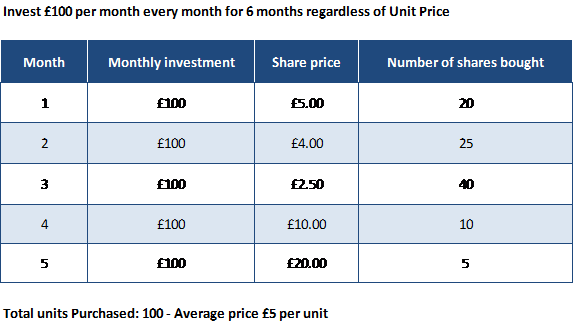

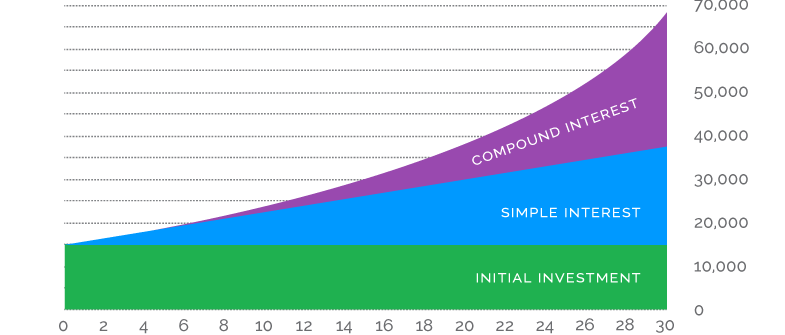

In order to retire early you need to become ’financially independent”. This means that you need to be able to live your life without the need to ‘earn a living’ through traditional employment. To achieve this there a few clear steps to take and a few key principles to understand. In this article I want to cover some of these steps and key principles as initial ‘food for thought’ for someone who is looking to achieve financial freedom. Even clever people are stupid when it comes to moneyIn schools we generally are not taught about finances. You may pick up a bit from parents, but then they haven’t been taught either and so bad habits and false assumptions are passed on and the lack of understanding is perpetuated from generation to generation. Maybe the truly wealthy are immune to this as they pay an army of accountants to help them look after their money. But for most people, this isn’t an option and if we want to understand money we need to look elsewhere. In the end it is down to all of us as individuals to learn about finances and increase our own ‘Financial Intelligence’. The fact that you are reading this means that you are probably ahead of most people. This article isn’t going to cover everything though. It’s not even going to cover ‘a lot’! It will only skim over a few principles as a starting point. If you really want to improve your Financial Intelligence you will have to do a lot more research, and check out some reliable sources to ensure that what you learn is balanced and accurate. Don't fall in to the 'Debt Trap'!We seem to accept debt as ‘normal’ these days. People talk about how great their credit score is and how much credit they can get on their credit cards as if it’s something to aspire to. But is spending beyond your means really a great way to become financially independent? Or does this just generate the illusion of wealth? Buying ‘stuff’ on credit usually means you are paying interest on top of whatever you have bought, and the interest you end up paying can be quite considerable. If you have high interest debt then this is particularly true. Expensive credit card debt or car loans at a higher interest rate than you can achieve through passive income (see later) will mean that you are taking one step forward and two steps back. One exception to this could be a mortgage debt, if it is at a rate of below 4%. This is because the money you owe through your mortgage might be better utilised as an investment earning a rate above 4%. However, this isn’t clear cut, as paying off a mortgage can be a great weight lifted. The monthly repayments are usually one of your largest regular monthly outgoings, and reducing this can in itself be a great step towards ‘financial independence’.  'You can’t have money, and spend it'Whilst some people in well paying jobs seem to have a lot of money, many of them don’t as they also spend a lot of money. As I was told as a boy, ‘You can’t have money, and spend it’. They may be earning a lot, but they probably have little invested and live from payday to payday in the same way that many others do. They may believe that their primary residence, their home, is where their money is invested, and to some extent this is true. However, to release that money, they need to first sell their home, which isn’t always easy and never guaranteed to turn a profit. A key step to Financial Independence is to start thinking about where your money is spent. Call it a budget, a financial plan or whatever. But you need to start looking. It could just be a sheet of paper with a list of everything you have spent money on over the last 12 months. It's all there, in your bank and credit card statements - get them out, and make a list. Then look what can be cut and where you can save some money. You need to free up some spare money in order to be able to invest. The rich buy assets, the poor buy liabilitiesDid you know, that rich people don’t actually work for money? Rich people get money working for them. This is where it’s important to know the difference between an asset and a liability. There are plenty of complex definitions for these that you can look up on the internet. But in a nutshell, an asset is something that will generate money and a liability is something that will lose money. If you want to become financially independent then you need to focus on buying assets and not liabilities. Use the money you freed up when you did your budget to buy and hold assets. Keep buying them, month in month out. Remember to always ‘pay yourself first’. By this I mean you should be investing this money first before dealing with your other bills. Think about setting up a direct debit each month so that it happens automatically. This is how you get your money working for you. Your assets will produce passive income (you don’t have to work to earn it), and as your assets grow, so does the amount of passive income you earn. Every pound you invest in assets is a pound working for you. Leave it alone and it will continue working for you. Don’t focus so much on how much you are earning from your day to day job. Focus instead on how large your asset portfolio is and how much it is growing. This is your own ‘business’ and you need to look after it first and foremost. So what assets should you be buying? Well, that is up to you. One of the easiest assets to buy these days are funds that invest in shares and bonds on the stock market. This can be done through online brokers such as Freetrade* or Hargreaves Lansdown (other brokers are available).  Pound Cost AveragingYou may be aware that the stock market goes up and down and so you often see the phrase that investments may go down and you may not get back as much as you put in. This is something that I believe puts some people off investing. However, historically this has only ever been true when investing for the short term. If you truly believe that owning income producing assets is the path to financial freedom, then why would you sell them? You are in for the long term and when you look at longer term trends, the stock market has done very well. One way to also help with the ups and downs of the stock market is through ‘pound cost averaging’ - by investing on a regular basis, such as monthly, you will buy more when the cost is low and less when the cost is high. This smooths out some of the ups and downs in the market and means that overall you are buying at an ‘average’ cost. Small and often is the way to go!  Failing to plan is planning to failWhen you do start to buy assets, don’t just invest based purely on the opinions of others. If you do, you will be pulled all over the place as different people will give conflicting advice based on what they believe your priorities should be. Be clear on what you want to own and why. As an example, my assets generally produce an income in the form of interest or a company dividend. For me that is important as I want a regular income now. If you are currently in employment, and don’t yet need to receive a regular income from your assets, then a different set of assets may be more appropriate, such as high growth accumulation funds (accumulation funds automatically reinvest any earnings back into the fund which results in compound interest). You can always then switch these when your objectives change and you want to start releasing the income. So, have a plan, know why you are investing, what your objectives are, both in the short and long term, and be clear on what you want to invest in. ‘Compound Interest is the eighth wonder of the world. He who understands it earns it, he who doesn’t, pays it’ (Albert Einstein)Most people are familiar with the concept of earning interest. You put money in the bank and they pay you a bit of interest each month. It’s usually pitifully low and doesn’t keep up with inflation and so in reality you are losing money. But that’s another story! Well, compound interest is where any interest you earn is paid back into your ‘savings’ and so the following month you not only earn interest on your original sum, but you also earn interest on the previous months interest. In the short term, this isn’t that significant. However, in the long term, this compounding really makes a huge difference. This means that the money you invest in your 20s and 30s is so much more important than money you invest in your 40s and 50s. Small amounts invested when you are young become surprisingly large when you are older. Compound interest and time are very important concepts for long term investing. In the graph below you can clearly see that compounding the interest over 30 years has nearly doubled the value of the investment compared to just simple interest.  Prepare for the WorstTo make sure that your plans stay on track you should always have a contingency plan. Occasionally things go wrong. Your car unexpectedly breaks down, or you lose your job. Being prepared for these events mean that your plans are not thrown into disarray! One way to do this is to have an emergency cash fund. Many people suggest 3 to 6 months of living expenses is the right amount (unless you are retired in which case 1 to 3 years is recommended). But really, again, it is up to you how much you have in your emergency fund. Some of this should be in easy access accounts so that you can use it immediately if needed. But you could have some saved in fixed term accounts to give you a bit more interest (as easy access accounts pay very poor interest rates). One of the tricks that I employ is to ‘ladder’ my savings. As an example, say your emergency fund is £10,000. You could keep £4000 in an easy access account which is likely to be enough for most emergencies that require immediate funds. You could then save the rest in a series of 1 year fixed rate savings accounts, say £500 each month. Then after 12 months, your first fixed rate account matures and £500 is released. This can then be put back into another 12 month fixed rate account if not needed or used as part of your contingency plans if necessary. Each month another £500 is released and so on. Diversify your AssetsDifferent assets will do well at different times. It therefore makes a lot of sense to hold a variety of different assets. If one asset is performing poorly in a particular year, another one will compensate by doing better. Diversification should be on both asset types and geography. So if you are invested in the stock market, you can have assets that hold equities (company shares) and assets that hold bonds (company IOUs). Both of these are also available across the world, and so when the U.S. is doing well, Europe might be going through a slump. There are thousands of different assets available and only you can decide which ones are right for you. But once you have a plan and know what you want to buy, make sure you have enough diversification so that any dips in the value of your assets are smoothed out. So, in summary….Spend the time you need to learn about finances so that you can make the right financial decisions. Pay off your debt and make a budget/financial plan so that you know where you are spending your money and where you can make savings. Buy assets on a regular basis that will provide income over the long term. Minimise risk through diversification and keep an emergency fund in easily accessible cash. At some point, your income producing assets will provide you with enough income that you no longer need to worry about working for someone else. You are now Financially Independent!

0 Comments

A lot of companies these days will provide you with a mobile phone, as part of the tech you need to effectively do your job. Having a mobile phone will allow you to keep in contact with colleagues and customers alike, through calls, texts, messaging apps and email. However, when you finish work for the day, or for the week, do you then turn off your work phone? Or do you, like many, keep it on so that family and friends can contact you outside of work hours? Having a work phone that you can use for both work and private can save you a fair bit of money as you don't need to buy your own phone and don't need to pay for your own contract. On the face of it, this seems like a real 'win', a free phone to be used as much as you like!

But now ask yourself the following questions; how often do you look at work emails outside of working hours? How often does a work colleague or customer call you when you are spending 'quality time' with the family? Is this really the best way to create a great 'work/life' balance? Do you find that it's sometimes difficult to 'switch off' and 'unwind'? There IS an alternative - get a second mobile phone for personal use. This doesn't have to cost you a lot as it doesn't have to be the newest all singing and dancing phone - just something that you have with you evenings, weekends and when on annual leave, so family and friends can contact you when your work phone is switched off and locked away. You can even buy a refurbished phone if you want, for example through Giffgaff, and then use a Pay As You Go (PAYG) sim - often much cheaper than getting a contract. Giffgaff also sell monthly bundles which they call 'Goodybags" starting from as little as £6 per month with unlimited calls and texts. It's a bit like a 1 month contract, but you can start and stop whenever you want. You can manage and monitor your usage via the handy Giffgaff mobile app and there is a great online community who can answer your questions quickly. And if you get a Giffgaff phone sim by clicking on the following link you will even get a £5 'thank you' as a bonus!

|

RSS Feed

RSS Feed